China’s Underserved Markets: A Multi-Billion Dollar Opening for Global Innovators

Introduction: Bridging the Gap in China’s New Economy

China’s rapid growth has left notable white spaces across its economy – untapped needs in technology, energy, compliance, and regions that savvy foreign entrants can fill. Analysts estimate tens of billions of dollars in opportunitiesacross these underserved sectors in the near term, with trillions in long-run potential driven by China’s green and digital transitions. For example, the World Bank projects China will require up to $17 trillion in green infrastructure and tech investment by 2060 to meet its climate goalsreuters.com. Likewise, the legal technology market – barely $1.8 billion in 2023 – is expected to double to $3.7 billion by 2030grandviewresearch.com, still under 10% of global spendgrandviewresearch.com and indicating vast room to grow. This article maps the major market gaps – from sectoral voids in legal tech, green energy, biotech, ESG and AI compliance, to business model voids like compliance SaaS and legal AI, to regional and policy openings – that together represent an estimated $100+ billion near-term prize. We also examine what these openings mean for foreign law firms, multinational general counsels, and strategic investors looking to enter or expand in China.

1. Sector Gaps: Underserved Industries from Legal Tech to Green Energy

Legal Technology & Services: China’s legal sector is modernizing quickly yet remains under-digitized in many areas. Investment in legal tech surged – over $1.2 billion flowed into Chinese legal tech startups in 2022hrone.com, and the market grew 38% last yearhrone.com – but adoption is uneven. Even after this growth, China’s legal tech market was just $1.8 billion in 2023, about 7.4% of global legal tech spendinggrandviewresearch.comgrandviewresearch.com. This signals a gap in advanced tools for contract management, e-discovery, and compliance. The upside is huge: by early 2024 the market hit $1.5 billion (a 26% jump from 2022)hrone.com, and it’s on pace to reach ~$3.7 billion by 2030grandviewresearch.com. Major initiatives are propelling this trend – from the Supreme People’s Court digitizing 90% of civil cases under its “Smart Court” programhrone.com, to 72% of top firms now using AI for contract analysis (boosting productivity ~40%)hrone.com. Still, vast swathes of legal work in China (especially for smaller firms and in-house teams) remain manual. Opportunity: foreign legal tech providers and alternative legal service firms can introduce proven solutions (AI document review, e-billing, etc.) tailored to China’s language and laws. Multinationals in China will demand these efficiencies, and domestic firms are warming to outsourcing routine tasks to focus on high-value counsel.

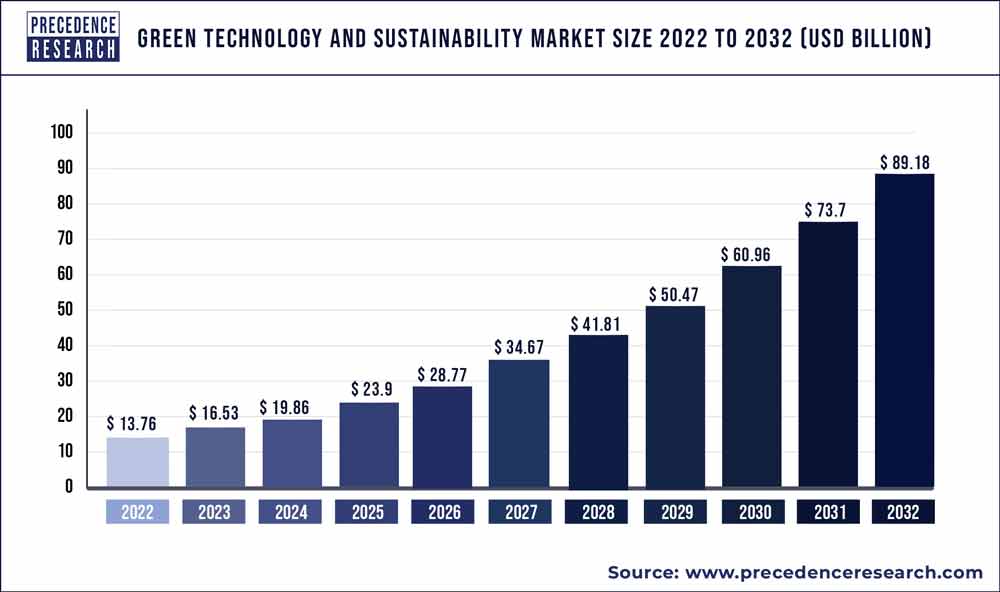

Green Energy & Climate Tech: China is a global leader in renewables, but rapid deployment has exposed infrastructure gaps. A blistering pace of solar and wind farm installations has outstripped storage and grid capacity, causing significant energy waste in some regions. In windy Inner Mongolia, 12% of wind power was curtailed (unused) in 2023and 10% of Qinghai’s solar output was wastedchina-briefing.com due to storage and grid constraints. Bridging this gap is essential: China aims for 50% of power from renewables by 2025china-briefing.com, which will require massive upgrades in energy storage, smart grid management, and carbon reduction tech. The energy storage market alone is set to explode – from 70 GW of capacity (worth $1.2 billion) in 2021 to 170 GW worth $6 billion by 2025china-briefing.com. By 2030, China plans to localize all core storage technologies and cut storage costs 30%china-briefing.comchina-briefing.com, aiming for 30+ GW of new non-hydro storage like hydrogen, batteries, and compressed airchina-briefing.comchina-briefing.com. This push creates openings for foreign cleantech firms – whether in grid-scale batteries, EV charging networks, hydrogen fuel, or carbon capture – to bring expertise and capital. Policy supports are strong: the 14th Five-Year Plan for Energy Storage explicitly welcomes market forces and independent service providers to investchina-briefing.com. With China needing trillions in green investment by mid-centuryreuters.com, foreign investors have a ripe chance to contribute technology and get a piece of an enormous pie, especially in areas like energy efficiency software, emissions monitoring, and carbon trading platforms that remain underdeveloped.

Biotech & Healthcare: China’s healthcare market is huge and growing, but domestic biotech innovation still lags in certain niches, representing an inviting gap. The government’s Healthy China 2030 agenda and aging demographics are driving demand for advanced therapies, yet China historically relied on imported drugs and medical devices. Today, local biotech is catching up – China is the world’s second-largest pharmaceutical market and its biopharma R&D spending is rising over 20% annuallyclinicaltrialsarena.com – but gaps persist in high-end drug development (e.g. mRNA vaccines, gene therapies) and global commercialization savvy. This is spurring cross-border partnerships: in the first quarter of 2025, 32% of global biotech out-licensing deal value came from Chinese companies, up from ~21% in prior yearsfiercebiotech.com. In other words, Chinese biotechs are increasingly seeking foreign partners to license or co-develop new drugs, filling their pipeline gaps with international innovation. Opportunity: foreign pharma and medtech firms can leverage these openings via joint ventures, R&D collaborations, and by supplying research services or critical technologies (for instance, specialized clinical trial platforms or manufacturing know-how) to Chinese players. Niche sectors like medical AI, telehealth, and elder care tech are also under-served – areas where foreign startups can pilot solutions in China’s vast healthcare system (with the right local partnerships and regulatory guidance from experienced counsel).

ESG & Compliance Services: As China’s regulators and trading partners turn up the heat on sustainability, ESG (Environmental, Social, Governance) compliance has leapt from obscurity to boardroom priority – but companies face a dearth of expertise and data. A recent survey found 76% of institutional investors cite lack of reliable, comparable ESG data in China as the #1 barrier to sustainable investmentdwtyzx6upklss.cloudfront.net. For overseas investors it’s even starker – 92% say poor ESG disclosure is a top challenge when evaluating Chinese firmsdwtyzx6upklss.cloudfront.net. Although more Chinese companies publish CSR reports nowadays, most lack standardized metrics and actionable detaildwtyzx6upklss.cloudfront.net. This information gap is an opportunity for service providers: there’s burgeoning demand for ESG rating agencies, carbon accounting software, green supply chain auditors, and legal advisers versed in ESG reporting frameworks. Notably, new disclosure mandates are on the horizon. Starting 2026, over 400 large Chinese companies will likely need to disclose ESG data under a pilot regulatory schemefiegenbaum.solutions. In finance, regulators are cracking down on greenwashing and pushing banks to measure climate risks. All of this creates a market for consultants and tech platforms that can help Chinese firms gather data (e.g. on emissions, labor standards), monitor compliance, and communicate transparently to global stakeholders. Foreign firms with experience navigating EU or US ESG regimes are well-positioned to fill this advisory gap, and foreign law firms can expect more clients seeking counsel on China’s evolving ESG and corporate social responsibility requirements.

AI Governance & Data Security: China’s tech industry is charging ahead in AI – from facial recognition to ChatGPT-like generative models – but governance and compliance systems around these technologies are playing catch-up. In 2023, China became one of the first countries to enact comprehensive generative AI regulations, issuing rules for AI services effective August 15, 2023reedsmith.com. These Generative AI Measures aim to balance innovation with security: they encourage investment in AI while imposing requirements on data privacy, content filtering, and transparencyreedsmith.comreedsmith.com. Crucially, the rules explicitly permit foreign-invested enterprises to develop and offer AI services in China, provided they comply with lawreedsmith.com. This policy tailwind opens the door for foreign AI firms (and their counsel) to establish China operations in areas like enterprise AI, provided they navigate the regulations. Nonetheless, compliance is complex – AI providers must implement security reviews, algorithm filings, and real-name user verification under various new lawschinalawtranslate.comreedsmith.com. Similarly, China’s data security and privacy laws (DSL and PIPL) now strictly govern cross-border data transfers. By early 2025, only 298 firms had completed the required security assessments for exporting data, with a mere 44 handling “important” data – and about 16% of those applications failed to pass musterhunton.comhunton.com. These numbers suggest many companies are still unprepared for China’s data rules, highlighting a gap in compliance solutions. Opportunity: firms that specialize in AI governance, cybersecurity, and data localization are in high demand. There is room for legal tech solutions that, for instance, automate personal data handling consent or conduct algorithmic audits. Pilot programs in China’s Free Trade Zones are even experimenting with “data negative lists” by industry to ease cross-border data flowshunton.com – an area where expert guidance is needed. Foreign legal counsel can add value by helping multinationals craft internal AI policies that meet Chinese regulations, or by guiding tech providers on ethical AI design that aligns with both Chinese and international norms.

2. Business Model Gaps: New Avenues in Compliance SaaS, Legal AI, and ALSPs

Beyond sector-specific voids, China’s market harbors business model gaps – promising service approaches and technologies that are proven elsewhere but nascent domestically:

- Compliance SaaS Platforms: Navigating China’s thicket of regulations – from export controls to cybersecurity audits – is a heavy lift, and many businesses still rely on manual tracking or ad-hoc consulting. This mirrors a gap seen globally a decade ago: the need for software-as-a-service solutions to manage compliance workflows. In China, this gap is acute in areas like data privacy (e.g. Personal Information Protection Law compliance), trade compliance, and regulatory reporting. For instance, companies now facing mandatory data transfer assessments must fill out complex filings and monitor data flows continuouslyhunton.com. A SaaS platform that automates such tasks (flagging risky transfers, compiling assessment documents, updating rules dynamically) can save tremendous time. We are starting to see entrants – for example, one U.S.-based data security firm offers an AI-driven tool to comply with China’s PIPL law, automating personal data discovery and transfer requestssecuriti.ai. But these offerings are still few. Opportunity: foreign SaaS providers can partner with local cloud operators to offer compliance management tools in China, or Chinese startups can fill the void domestically. Given authorities are releasing updated rules almost monthly in some domains, a cloud-based service that keeps companies continuously compliant is poised for demand.

- Legal Process Automation: While top-tier Chinese law firms have begun adopting AI and workflow tools, many routine legal processes in companies remain ripe for automation. There is a need for legal automation solutions – think automated contract drafting and analysis, AI-powered e-discovery, and online dispute resolution platforms – tailored to the Chinese context. Consider contract management: numerous multinational GCs in China still juggle contracts via email and Excel, lacking the kind of centralized contract lifecycle software common in the West. Similarly, compliance checks (e.g. anti-bribery due diligence, HR policy reviews) are often done manually. The impact of automation where it has been tried is telling: in a Deloitte China survey, 72% of major law firms reported using AI contract review tools, boosting productivity up to 40%hrone.com. However, that leaves a large segment of mid-tier firms and corporates not yet leveraging such tools – a gap that legal tech companies can target. Additionally, electronic litigation is gaining traction: China’s courts have piloted “Internet Courts” and smart case filing systems, but enterprises could benefit from automation on their side (e-filing systems, case management dashboards, etc.). Implication: Foreign legal automation vendors (from e-discovery providers to document assembly tools) should consider entering China via partnerships or JVs with local IT firms, ensuring data localization and adaptation to Chinese law. This can offer a differentiator for law firms and legal departments striving to do more with less amidst cost pressures.

- B2B Cross-Border Platforms: China is the world’s largest trading nation, yet cross-border B2B transactions – especially for SMEs – remain inefficient. There’s a gap for platforms that seamlessly connect Chinese businesses with foreign partners, handling not just matchmaking but also the compliance and logistics pain points of cross-border trade. Cross-border e-commerce has boomed on the consumer side: in 2022 China’s cross-border e-com trade topped ¥2 trillion (≈$280 billion) for the first timeenglish.www.gov.cn, doubling in just a few years. However, much of this is facilitated by big players (Alibaba, JD) and focused on retail goods. For B2B trade (industrial products, services, procurement), the ecosystem is less developed. For instance, a mid-sized manufacturer in Chengdu looking to export machinery or import specialized components faces fragmented channels, complex customs rules, and contract uncertainties. A digital platform that integrates trade matchmaking with built-in compliance checks, escrow payments, and cross-border contract enforcement could fill a real need. Moreover, China’s Belt and Road Initiative (BRI) is creating new corridors through Central and South Asia, increasing cross-border business with emerging markets – an area where neutral B2B platforms could thrive. Opportunity: foreign logistics and fintech players, in concert with Chinese partners, can build “one-stop” cross-border platforms (for supply-chain finance, customs clearance, etc.). Legal support for such platforms will be crucial, as they must navigate differing regulations in each jurisdiction. Law firms can find new work advising these platform ventures on regulatory licensing (e.g. e-payments, data export compliance) and on structuring terms that are enforceable across borders.

- Legal AI in Mandarin: The AI revolution in law has arrived, but Chinese-language legal AI tools are still in their infancy – a clear gap for innovation. Large Language Models (LLMs) like GPT-4 have shown impressive legal reasoning in English, yet when it comes to Chinese legal tasks, generic models fall shortarxiv.org. They struggle with local statutes, lack bilingual training, and pose data privacy concerns if using overseas APIs. Recognizing this, Chinese researchers only recently introduced “LawGPT” (2023), the first open-source Chinese legal LLMarxiv.org. LawGPT is specifically trained on Chinese law texts to improve its understanding of local statutes and case reasoning. Its emergence highlights both the demand and the nascency of this field – essentially no mature products yet. Implications: Foreign AI developers and legaltech startups can seize this moment to collaborate with Chinese firms on Mandarin legal AI solutions. Potential applications include AI legal assistants that corporate counsels can query in Chinese about regulatory changes, or bilingual contract review bots that flag compliance issues in both English and Chinese drafts. Given data sensitivity, on-premise or private-cloud deployments will be key (no company wants sensitive case data leaving China). Law firms too can benefit: those that invest early in custom Mandarin LLMs fine-tuned to specific practice areas (say, China’s tax law or labor law) will differentiate themselves in client service. In short, the playing field for legal AI in China is wide open – akin to the West ~5 years ago – offering first movers a chance to set the standard.

- Alternative Legal Service Providers (ALSPs): Around the world, ALSPs – firms offering legal services via new delivery models (outsourcing, managed services, flexible staffing) – have become a $28+ billion marketthomsonreuters.com, growing much faster than traditional law firms. In China, however, ALSPs are only just emerging, signalling a gap in the market for more cost-effective legal solutions. Historically, China’s legal market has been dominated by large domestic law firms and representative offices of international firms, with strict regulations on law practice ownership. That is starting to change: recent regulatory reforms allow foreign law firms to form joint ventures with local firms in pilot zonesgrandviewresearch.com, and the rise of Legal Process Outsourcing (LPO) is enabling routine work to be handled outside big firmsgrandviewresearch.com. For instance, document review or compliance monitoring that used to be done by expensive city law offices can now be offloaded to lower-cost centers or specialist firms. Yet awareness among clients about ALSP options – and the supply of credible ALSP providers in China – remains low. Opportunity: international ALSP players (the likes of Axiom, Elevate, Big Four-affiliated services, etc.) have an opening to expand in China, either independently (now that non-lawyer ownership rules have relaxed slightly) or via partnerships. They can offer Chinese corporates and foreign investors in China lower-cost solutions for e-discovery, due diligence, contract management, and temp legal staffing. Demand drivers are in place: corporate legal budgets in China are under pressure, and companies are grappling with “more compliance work, less headcount.” Even traditional Chinese law firms are seeing the value – some have started collaborating with ALSPs to handle high-volume tasks so their attorneys can focus on counselgrandviewresearch.comgrandviewresearch.com. For foreign law firms advising in China, incorporating ALSP strategies (either through affiliates or subcontracting) could be a strategic move to offer more competitive fees.

3. Investor Angle: M&A and Joint Ventures – Capitalizing on Value Gaps

For private equity, multinationals, and other investors eyeing China, these market gaps translate into concrete investment opportunities – if navigated shrewdly. After a slow 2022, China’s deal activity is cautiously rebounding: analysts forecast a notable M&A uptick in 2024 as economic conditions and policies improveiflr.com. Where are the openings?

- Distressed and Undervalued Sectors: China’s past few years saw intense regulatory crackdowns (in tech, education, real estate) that, while challenging, have created value opportunities. Certain sectors with strong fundamentals experienced sharp valuation drops due to policy shocks or cyclical downturns. For example, the consumer tech and online education industries lost billions in market cap after 2021 regulations – yet Chinese consumers’ demand for online services remains robust. Foreign investors with a long view are now cherry-picking in such areas: taking minority stakes in tech firms or acquiring spinoffs that focus on “clean” business models. Similarly, China’s property and infrastructure sector has been in distress, but high-quality commercial real estate or logistics assets in prime cities could be acquired at a discount. Another area is industrial and mobility tech: China’s push for electric vehicles and advanced manufacturing is unabated, even though some local EV startups and component makers face cash crunches. Savvy foreign funds (especially from the Middle East and Asia) have stepped in – recent deals include Abu Dhabi’s sovereign fund investing $739 million into EV maker NIOskadden.com, and Saudi Aramco acquiring 10% of Rongsheng Petrochemical for $3.4 billionskadden.comto secure a foothold in China’s refining market. These deals show that when valuations align with strategic interest, foreign capital is welcome. Implication for legal advisors: robust due diligence and regulatory risk assessment are key, as these “cheap” assets often come with compliance strings attached. Law firms should be prepared to navigate national security review processes (especially if acquiring tech assets) and to structure deals creatively (e.g. using trusts or minority positions) to get them approved.

- Strategic Joint Ventures: Heightened geopolitical tensions and China’s remaining investment restrictions mean outright acquisitions aren’t always possible – but joint ventures (JVs) and strategic partnerships can fill the gap. In fact, rising US-China tensions may encourage more JVs in less sensitive sectorsskadden.com, as companies seek growth while managing risk. We see this in the automotive arena: in 2023, China’s Geely and France’s Renault formed a global JV spanning Europe and China to develop hybrid powertrainsskadden.com – a structure that lets both sides share tech and market access. JVs are also a favored route in sectors where foreign ownership was limited (and even as those limits lift, local partners provide government relationship value). For instance, foreign asset managers often team with a Chinese bank or fintech firm to tap China’s wealth management market. With the government dropping foreign equity caps in financial services and manufacturing recentlyenglish.www.gov.cn, the field is more open for majority-foreign JVs, but having a strong local junior partner can ease execution. Opportunity: foreign firms can negotiate JVs in emerging fields like AI and semiconductors (where China is keen to gain know-how but also wary of full foreign control) or in healthcare services (where local hospital networks team with foreign medical operators). The Free Trade Zones provide a playground for innovative JV structures – e.g. in Hainan, healthcare JVs benefit from looser licensing rules and tax breaks. Lawyers will play a crucial role in structuring these JVs to align with China’s regulations (which often require JV contracts to include specific governance and Communist Party committee provisions), while protecting foreign IP and ensuring profit repatriation mechanisms.

- Free Trade Zone Entry Points: China’s Free Trade Zones (FTZs) – especially the high-profile Hainan Free Trade Port and Shanghai FTZ – offer investors streamlined entry pathways and incentives that directly address some market gaps. Hainan, in particular, is being positioned as a new gateway for foreign investment. By end of 2024, Hainan boasted 9,979 foreign-invested enterprises, 77% of which were established after June 2020 when the free port plan launchedenglish.www.gov.cn. This surge reflects Hainan’s generous policies: zero tariffs on many goods, 15% flat tax rates for eligible foreign companies and executivestrade.gov, and a goal of independent customs operations by end-2025 to enable unfettered flows of goods and dataenglish.www.gov.cnenglish.www.gov.cn. Notably, Hainan’s Free Trade Account system lets companies freely exchange RMB and foreign currency – a boon for investors frustrated by China’s usual capital controlstrade.gov. Meanwhile, the Shanghai FTZ, launched in 2013, pioneered reforms like negative lists (identifying restricted sectors) and easier business registration; it continues to pilot financial liberalizations (e.g. freer yuan convertibility) that facilitate foreign firms’ China operations. Other FTZs – Shenzhen Qianhai, Guangzhou Nansha, Tianjin, etc. – focus on specific themes from high-tech to e-commerce. Opportunity: Investors can leverage FTZs as launch pads for new ventures that might be harder elsewhere in China. For example, a foreign cloud computing provider could set up in the Hainan FTZ to take advantage of more relaxed data rules and incentives, before expanding nationwide. Free Trade Zones also allow experimenting with business models (like wholly foreign-owned training centers or senior care facilities) that align with gap areas we discussed. Legal counsel should familiarize clients with the nuances of each FTZ’s policies – e.g. Hainan has its own foreign investment negative listinvestmentpolicy.unctad.org and unique rules like QDLP/QFLP schemes for fund investorstrade.gov. Structuring an investment via an FTZ entity can mean the difference between a green light and a quagmire, especially for industries still sensitive on the national level.

- Sectors with Strong Fundamentals but Policy Tailwinds: Another way to identify gaps is to look for sectors that Beijing is heavily promoting for long-term stability or strategic needs, but where current private investment is lagging. For instance, green tech manufacturing (solar panels, EV batteries) is one – China leads production globally, yet certain sub-segments are fragmented or facing overcapacity, inviting foreign strategic investment to consolidate and upgrade quality. The agritech/food security area is similar: China wants to boost food productivity and has policy support for agritech, but the sector lacks capital and advanced technology – foreign agri-businesses can fill the gap via investments in seed technology, supply chain logistics, or food processing JVs. Financial services is yet another: foreign banks and insurers were historically capped at minority stakes, but now those caps are goneenglish.www.gov.cn; this coincides with a time when Chinese consumers’ needs (for retirement products, sophisticated banking services) are outpacing what domestic institutions offer. Thus, firms that bring in new financial products (insurance tech, asset management expertise) can capture an underserved client base. Backing from policy is clear – the government has completely removed foreign investment limits in the manufacturing sector and cut the nationwide negative list to just 29 restricted areasenglish.www.gov.cnenglish.www.gov.cn, the most open stance in decades, reflecting an intent to attract FDI into high-tech and advanced industries. Even data flows, once a strict area, are seeing easing proposals (e.g. draft rules in 2023 to simplify cross-border data transfer approvals for less sensitive dataskadden.com). All these are positive signals for investors: the policy winds are at your back if you choose a sector aligned with China’s priorities. The key is still careful deal planning – ensuring compliance with any remaining foreign ownership rules, and structuring investments to qualify for incentives (such as setting up in a specific province that offers subsidies for that industry).

In summary, while investors must remain mindful of regulatory and geopolitical risks, China’s market gaps present a target-rich environment for M&A, minority stakes, and joint ventures. Those who pick the right spot – a sector with unmet demand and policy support – and execute with strong local knowledge can secure valuable footholds in the world’s second-largest economy at a time when competition may be less intense than during past boom years.

4. Geographic Hot Zones: Beyond Beijing and Shanghai – Tapping Regional Upside

Much of China’s untapped opportunity lies outside the megacities, in regions and cities that have come of age economically but remain underserviced. Foreign firms and investors traditionally flocked to Tier-1 hubs (Beijing, Shanghai, Shenzhen, Guangzhou). Now, Tier 2 and 3 cities, western provinces, and specialized zones are the new frontiers.

Rise of Inland Markets (Tier-2/3 Cities & Central-Western Provinces): Cities like Chengdu, Chongqing, Xi’an, Wuhan, Hefei – once considered backwaters for FDI – have transformed into thriving economies with populations the size of small countries. They boast growing middle classes, universities churning out talent, and local governments eager to court foreign business. A 2024 survey of multinational executives found 77% consider China’s central and western regions as potential markets for their products/services, and nearly half see them as potential production basespwccn.com. Over 70% of MNCs surveyed had at least evaluated doing business in those inland areaspwccn.com, attracted by factors like lower labor and land costs, large untapped consumer pools, and improved transport linkspwccn.com. These regions are now “on the radar” – in fact, 30% of multinationals in the survey called the central/west a “big opportunity” or even “game-changing” for their China strategypwccn.com. Specific hot zones include: Chengdu-Chongqing, a twin-city economic circle driving growth in the southwest; Wuhan, rebounding as a high-tech and auto manufacturing base in central China; Xiangtan and Changsha in Hunan, emerging in advanced manufacturing; Zhengzhou in Henan, a logistics and e-commerce hub leveraging its railway links. Moreover, these inland provinces tie into the Belt & Road Initiative (BRI) – e.g. Chongqing and Xi’an are key rail termini for China-Europe freight trains, making them crucial nodes for trade with Central Asia and Europe. Indeed, about 21% of companies view central/west provinces as vital land bridges to South & Central Asia, and 20% see them as logistics hubs for Chinapwccn.com. Opportunity: Foreign firms in sectors like retail, healthcare, education, and industrial equipment can expand into these cities where competition is thinner and local governments may grant incentives. Law firms may consider establishing branch offices or alliances in regional centers to capture the rising deal flow – for instance, supporting a European manufacturer opening a factory in Chengdu, or advising a tech JV in Xi’an’s software park. Key to success will be adapting to local dynamics: navigating provincial regulations (which can differ from Beijing’s), building relationships with municipal authorities, and finding reliable local partners. Firms that make the effort can become first-movers in markets that may be tomorrow’s Tier-1 cities.

Western Provinces & BRI Infrastructure: China’s far-west provinces (like Xinjiang, Gansu, Yunnan, Guangxi, Ningxia) historically lagged the coast but are now strategic links in the Belt and Road and targets of Beijing’s “Western Development” drive. Massive infrastructure projects – highways, railways, pipelines – are underway to connect these provinces with neighboring countries. For instance, Yunnan is a gateway to Southeast Asia (bordering Vietnam, Laos, Myanmar) and has new transport corridors, while Xinjiang is positioned as the Silk Road hub into Central Asia. These regions have abundant resources and strategic location but lack advanced services and investment. Opportunity: foreign companies can participate in BRI-related projects (providing engineering, project finance, or legal structuring expertise) and tap new consumer markets as these provinces develop. Tourism, logistics, clean energy, and agribusiness are promising sectors in the west. For example, international hotel chains and agri processors are now looking at Xinjiang and Gansu as the government improves security and infrastructure there. Western provinces often offer tax breaks and easier permitting for foreign investors to attract capital. However, they also come with risks – the regulatory environment may be less predictable and, in some cases, there are U.S./EU sanctions considerations (e.g. Xinjiang). Thus, companies should proceed with counsel to ensure compliance with all applicable laws when operating in sensitive western regions.

Free Trade Zones – Hainan and Beyond: We touched on Hainan Free Trade Port in the investor section, but it’s worth emphasizing as a geographic opportunity zone. Hainan, a tropical island the size of a small province, is being turned into China’s largest special economic zone with unparalleled openness. By 2025, Hainan will adopt independent customs – essentially operating outside China’s regular customs regime – enabling zero-tariff imports, duty-free shopping, and free flow of data and capital within the islandenglish.www.gov.cnenglish.www.gov.cn. The goal is to make Hainan a combination of Hong Kong (a free port) and Singapore (a financial center) on Chinese soil. Already, the surge in foreign enterprises setting up in Hainan (nearly 10,000 as of 2024) shows that many view it as a beachhead for China businessenglish.www.gov.cn. Key sectors Hainan targets: tourism, high-end consumer goods (with its booming duty-free malls), healthcare (it’s permitting foreign-owned hospitals and clinics), finance (experimenting with fintech and fund vehicles), and aerospace/tech (the Wenchang spaceport and related tech parks). Foreign law firms and consultants are also establishing offices to service the influx of investors. For businesses that hesitated to enter China due to bureaucratic hurdles, Hainan offers a more flexible environment – e.g. streamlined customs clearance, a simplified tax regime (15% flat corporate tax)trade.gov, and easier cross-border money transfers via free trade accountstrade.gov. It’s a prime location for regional headquarters or innovation centers targeting Asia. Apart from Hainan, the original Shanghai FTZ and newer zones in Guangdong, Fujian, Tianjin, etc., remain vital. Shanghai FTZ has been expanded to include Lingang (a new area focusing on high-tech manufacturing and offshore trade). Shenzhen’s Qianhai FTZ focuses on finance and collaboration with Hong Kong, offering opportunities in fintech, asset management, and legal services (foreign law firms can operate more freely in Qianhai via joint operations). Zhoushan FTZ in Zhejiang specializes in commodities trading (oil, LNG) and shipbuilding, inviting energy traders and maritime firms. Each FTZ has its niche, but all share a mission to pilot policies that make doing business easier – meaning foreign investors can often enjoy faster incorporation, more liberal foreign exchange rules, and pilot programs (like relaxed telecom regulations or expanded e-commerce licenses) in these zones. Implication: Companies should evaluate if their China entry or expansion could be routed through an FTZ to capitalize on these benefits. Legal counsel can assist by comparing the specific incentives and regulatory flexibilities of each zone and securing any special qualifications needed to register there. For instance, certain zones allow wholly foreign-owned enterprises in sectors that are restricted elsewhere – knowing these details can be a competitive advantage.

In short, geography in China is no longer just a tale of Beijing and Shanghai. The smart money is diversifying across the country’s “next 100 cities” and strategic regions. Those who establish a presence in these hot zones now – be it a sales office in a booming inland city or a factory in a free trade port – stand to ride the next wave of China’s growth, often with generous local support and far less foreign rivalry.

5. Policy Tailwinds: Legal Reforms and Liberalization Bolstering Market Entry

China’s evolving regulatory landscape – often perceived as a barrier – is, in many respects, becoming a tailwind for would-be entrants by clarifying rules and opening sectors. Several recent policy shifts bode well for foreign businesses and investors aiming to fill the gaps we’ve discussed:

- Foreign Investment Reforms: China has made tangible strides in liberalizing foreign investment rules. The clearest indicator is the shrinking of the “Negative List” – the list of sectors off-limits or restricted for foreign capital. In 2020, a new Foreign Investment Law came into effect promising equal treatment for foreign firms; since then, the negative list has been cut year by year. By 2024, the nationwide negative list was down to just 29 items(from over 100 a few years prior), and China “completely removed foreign investment access restrictions in manufacturing”english.www.gov.cn. This means virtually all manufacturing sub-sectors – including autos, where the last joint-venture requirements on EVs were scrapped – are open to 100% foreign ownership. Restrictions in areas like finance and agriculture have also been eased. Result: foreign companies can now enter more industries outright, or negotiate higher stakes in JVs than before. Additionally, Beijing has pledged national treatment for foreign firms in areas like government procurement and licensingenglish.www.gov.cn, aiming to level the playing field. These reforms increase the viability of market entry because they reduce the regulatory uncertainty and equity limitations that previously deterred some investors.

- Pro-Innovation Regulations (AI, Tech): Rather than banning new tech, China is moving to regulate it in a pro-growth way. The Generative AI Measures of 2023, for instance, not only impose compliance obligations but also explicitly encourage “independent innovation in key AI technologies” and international cooperation on AIreedsmith.com. The policy sends a message that compliant AI development – even by foreign players – is welcomed. Similarly, China’s data laws, while strict, are maturing toward workable solutions: in early 2025 regulators proposed easing cross-border data transfer controls (exempting certain low-risk data from onerous approval)skadden.com, responding to industry feedback that innovation requires data flow. Meanwhile, intellectual property (IP) protections have strengthened (specialized IP courts, increased damages for infringement), a reform that gives foreign tech firms more confidence to bring know-how into China. For law firms and GCs, these developments mean the advisory focus shifts from “Can we do this in China?” to “How do we do this compliantly in China?” – a more manageable question. Companies that stay abreast of the latest regulations – for example, draft AI laws, algorithm registries, or open-source software rules – and engage proactively with regulators can actually shape the emerging frameworks. The tailwind here is that the government’s goal is not to stifle tech but to guide it, so those willing to play by the rules can still thrive.

- Labor Law Enforcement & Talent Trends: In a somewhat paradoxical way, stricter labor law enforcement in China can benefit high-compliance foreign firms by leveling the playing field on costs and improving workforce sustainability. Over the past year, Beijing launched a high-profile crackdown on excessive overtime (the “996” culture), declaring such practices illegal and ordering companies to comply with the statutory 44-hour workweek and overtime pay requirementsharris-sliwoski.comharris-sliwoski.com. Tech giants like Tencent and Alibaba publicly rolled back overtime, and regulators have made examples of companies flouting the rulesharris-sliwoski.comharris-sliwoski.com. While this increases labor compliance burdens, it also reins in local competitors who may have gained advantage through overworking staff. Foreign multinationals, which typically already abide by global labor standards, no longer face a situation where respecting work-life balance means losing ground on productivity – the law now mandates everyone follow suit. Additionally, these labor moves tie into China’s “common prosperity” agenda and efforts to spur domestic consumption (happier, rested workers spend more), which is positive for market growth. Another trend is the improvement of vocational education and skilled labor pools in interior regions, thanks to government programs – easing one challenge foreign firms often cited: talent availability outside Tier-1 cities. In sum, a more regulated labor environment and broader talent base make it easier for foreign companies to expand in China without facing severe HR headaches or PR risks (like being called out for labor abuses). Of course, companies must vigilantly update their policies – ensuring all China operations rigorously record working hours, pay proper overtime (150–200% of wages)harris-sliwoski.com, and comply with social insurance. Law firms are already busy helping clients audit their practices, as a single employee complaint can trigger investigations under the new regimeharris-sliwoski.comharris-sliwoski.com. But ultimately, those who invest in compliance will find a more stable operating environment, supported by authorities’ vision of sustainable development.

- Financial and Capital Market Liberalization: China continues to open its financial sector and make capital flows more convenient, which greases the wheels for foreign investment. All foreign ownership caps in securities, asset management, futures, life insurance, and banking have been removed in recent years, allowing firms like JPMorgan, BlackRock, and UBS to take full control of China units. The impact is twofold: foreign financial firms can tap China’s huge market directly, and Chinese companies gain greater access to global expertise and capital. On the capital flow side, pilot programs are expanding. We discussed Hainan’s free trade accounts enabling free currency exchangetrade.gov. Additionally, schemes like Shanghai’s QDLP (Qualified Domestic Limited Partner) and Beijing’s QFLP (Qualified Foreign Limited Partner) let foreign and Chinese funds invest across borders more freely by relaxing quota and registration requirementstrade.gov. The Stock Connect and Bond Connect programs link Hong Kong’s markets with the mainland, making it easier for foreigners to invest in Chinese stocks/bonds and vice versa. There’s also been progress on easing profit repatriation – SAFE (China’s forex regulator) has simplified some procedures for foreign firms to remit dividends. Implication: these measures reduce the friction that often deterred medium-sized foreign businesses. A German Mittelstand company, for instance, can be more confident that if they set up a China subsidiary, they can eventually repatriate earnings, or that they can raise RMB funds locally if needed. And for foreign private equity, the ability to actually exit investments (via IPO on a Chinese exchange, or sale to a local buyer who can get financing) is improving with capital market reforms. This positive momentum in financial liberalization complements the sectoral openings – making the overall ecosystem more foreign-investor-friendly than it was a decade ago. Professional advisors will still need to guide clients through the paperwork (e.g. registering for the latest cross-border facilitation pilot), but at least now the policies are written to support, not hinder, compliant financial flows.

In essence, China’s policy environment in 2025 is increasingly oriented toward stable growth and high-quality foreign participation, after a period of tumult. Legal reforms and guidelines – from foreign investment laws to digital economy regulations – are providing clearer goalposts. For foreign firms and their counsel, the takeaway is to stay updated and engaged: a door closed last year may be open now, thanks to a new policy, and early movers will benefit most from incentives and goodwill. Those who demonstrate alignment with China’s policy goals (be it green development, tech innovation, or social harmony in labor practices) can leverage these tailwinds to enter gaps that previously would have been too risky or restricted.

Implications for Foreign Legal Counsel: Guiding Clients to Opportunity

For foreign law firms and in-house legal teams of multinationals, the trends discussed above are not abstract – they directly shape the advice and services you must provide in China. As market gaps turn into tangible projects and deals, legal counsel will be at the forefront of navigating entry strategies, ensuring compliance, and structuring partnerships. Here are key implications and actionable insights:

- Advising on Sector Opportunities: Legal teams should proactively identify which of the highlighted gap sectors align with their clients’ goals and educate clients on the evolving regulatory frameworks. For instance, if you have a renewable energy client, you might brief them on the new energy storage incentives and grid reform policies, paving the way for a China market entry plan. If your corporate client is exploring digital solutions, explain how China’s legal tech landscape is opening – perhaps suggest a partnership with a Chinese legaltech startup (with IP safeguards drafted) to localize their product. Essentially, lawyers should act as market intelligence conduits, translating China’s legal developments into business strategy. Publishing client alerts or hosting webinars on topics like “New ESG disclosure rules in China” or “Opportunities in China’s AI regulation era” can position your firm as a thought leader and attract clients interested in those gaps.

- Structuring for Success (JVs, FTZ entities, M&A due diligence): Many opportunities will involve complex structuring – be it forming a joint venture, establishing an FTZ subsidiary, or acquiring a Chinese target. Foreign counsel must design structures that both seize the opportunity and mitigate risk. For example, if a client is considering a JV to enter a sensitive tech sector, you’ll need to draft agreements that secure the client’s IP and control over tech transfer, while complying with Chinese JV laws (which may require board seats for the local partner or Party committee clauses). If a client opts for an FTZ entity to test the waters, you’ll handle the entity setup under that zone’s rules and ensure any preferential treatments (tax breaks, relaxed licensing) are contractually recognized and long-term where possible. In acquisitions, robust due diligence is paramount: counsel should focus on regulatory compliance of the target (any hidden data transfer violations? labor disputes under the new overtime rules? environmental non-compliance that could scuttle an ESG-minded investor?). We also need to be creative: some gaps may require navigating around rules – e.g. using a VIE (variable interest entity) structure if an industry is still restricted, or leveraging Hong Kong/Macau CEPA provisions for certain service sectors. Expert local advice and relationships with Chinese firms will enhance foreign counsel’s ability to craft workable solutions.

- Compliance and Risk Management as Competitive Advantage: With China’s regulatory enforcement tightening (data, labor, anti-monopoly, etc.), foreign companies will look to their lawyers not just to get in, but to stay out of trouble. Emphasize building strong compliance programs as a selling point – e.g. help clients implement rigorous data governance frameworks to deal with PIPL, set up whistleblower channels and training to comply with the anti-996 labor directives, and align with global ESG best practices to pre-empt local scrutiny. Foreign counsel should coordinate with local Chinese counsel to conduct compliance audits for clients, identifying gaps before regulators do. Those law firms that can seamlessly handle cross-border compliance (for example, ensuring a client’s China operations meet both PRC and EU data privacy standards) will be highly valued. In essence, being the bridge that helps clients meet East and West regulations can cement long-term advisory relationships. Moreover, in deal-making, assessing political/regulatory risk (like CFIUS-type concerns or China’s own national security review) is now a standard part of legal due diligence – counsel should build expertise in these processes to guide deals to approval.

- Leveraging Technology and ALSPs: Ironically, the same gaps in legal tech and ALSP services in China that we identified are also opportunities for foreign law firms to improve their own service delivery. Forward-looking firms are beginning to deploy AI and automation internally for China-related work – for example, using translation AI to quickly review Chinese documents, or employing contract analytics to handle high-volume contract localization. If Chinese legal AI tools are limited, foreign firms might adapt their in-house tools (under strict data control) to fill the void, thereby serving clients faster and more cost-effectively. Likewise, exploring partnerships with or even creating an ALSP arm in China (taking advantage of regulatory easing for law firm JV/operations) could allow your firm to capture work that clients would otherwise not send due to cost – e.g. high-volume contract review in Mandarin, due diligence on local supply contracts, etc. By offering these alternative services, foreign firms can not only tap a new revenue stream but also guard against local competitors undercutting them on price for commoditized work. Essentially, practice what we preach: use innovation to tackle China’s legal market gap – it will resonate with clients who are doing the same in their industries.

- Policy Advocacy and Engagement: Finally, foreign legal counsel – especially those in international firms or industry coalitions – have a role in shaping the environment. Engaging with Chinese regulators through comments on draft laws, participating in foreign chamber of commerce committees, and maintaining dialogue with policy stakeholders can give your clients a voice and glean insights. For instance, if China is drafting a new AI law, submitting constructive feedback (perhaps informed by the EU AI Act experience) not only helps shape a workable law but positions your firm as a go-to advisor on that topic. Similarly, keeping close to U.S., European, and other home country regulatory shifts vis-à-vis China (export controls, sanctions, etc.) is vital so you can counsel clients on how to invest in China without falling afoul of their home regulations. The best counsel will offer a 360-degree view – identifying the sweet spot where a foreign company can operate in China’s gaps with both Chinese policy support and home country compliance. That kind of guidance turns legal counsel into strategic advisors, not mere translators of law.

Strategic Recommendations: Capturing the Emerging Gaps

In conclusion, China’s market gaps present a rare strategic opening for foreign businesses and their advisors – but to capture these opportunities, a proactive and well-informed approach is essential. Here are key recommendations for foreign firms aiming to capitalize on China’s underserved sectors and investment flows:

- Align with China’s Policy Priorities: Tailor your market entry to sectors that China is promoting (green tech, advanced manufacturing, digitalization, healthcare). Beijing’s backing means easier approvals and sometimes incentives. For example, if you’re a renewable energy company, frame your investment as helping China meet its 2060 carbon-neutral goal (with data on how your technology increases efficiency). Use the latest Five-Year Plan and local government industrial plans as guideposts – positioning your offering as filling the gaps those plans identify.

- Leverage Entry Platforms (FTZs, JVs, Partnerships): Reduce risk by using China’s sandbox zones and willing local partners. Set up in Free Trade Zones like Hainan, Shanghai FTZ, or others relevant to your industry to benefit from streamlined regulations – e.g. a fintech firm might choose Shenzhen Qianhai for its favorable finance rules. Consider joint ventures or strategic alliances in sectors where local insight or networks are critical (or where rules still require a Chinese partner). The right partner can accelerate market penetration and help navigate informal hurdles. Conduct thorough partner due diligence, and structure agreements to allow flexibility (clear exit clauses, phased equity increases as rules allow). Partnerships can also be with local governments or universities – for instance, a biotech company could partner with a Chinese university in a west province to establish a research center, tapping talent and securing goodwill.

- Differentiate with Compliance and Quality: China’s market is competitive, but many incumbents falter on compliance (e.g. data protection, environmental standards) and quality control. Foreign entrants should turn this into a selling point. Implement gold-standard compliance programs from day one – not only to avoid fines but to win trust from customers and authorities. For example, a foreign food processing firm entering western China could highlight its world-class food safety processes, positioning it as a premium and reliable choice amid domestic food safety scandals. Likewise, ensure your product or service truly fills the gap on quality: if launching a SaaS platform, localize it fully to Mandarin and Chinese laws (perhaps even get voluntary certification from a Chinese authority), showing you go beyond what’s required. Over-engineer data security if you’re in tech – given recent data breaches in China, customers will appreciate the rigor. By being the most compliant and high-quality player, foreign firms can capture clients who are now highly sensitive to risk (including state-owned enterprises that have been told to prioritize secure and compliant vendors).

- Invest in Local Talent and Knowledge: To succeed in Tier-2 cities or niche sectors, you need on-the-ground expertise. Hire and empower local teams – not just sales, but also government relations and compliance experts who know the local dialect (figuratively and literally). If you’re targeting multiple regions, consider regional hubs (e.g. Chengdu for southwest, Wuhan for central China) with dedicated teams rather than trying to manage everything from Shanghai. Provide training and growth paths to retain top Chinese talent; their guanxi (relationships) and understanding of local consumer behavior or business culture will be invaluable in exploiting gaps. For foreign law firms, this means recruiting experienced PRC-qualified lawyers or even pursuing the Sino-foreign law firm joint operation models now permitted, to offer integrated local-law advice. Also prioritize knowledge development: keep track of local regulations, subsidy programs, and enforcement trends across provinces – they can differ markedly. A company that stays ahead of a provincial policy change (say a new green standard in Shandong or a data rule in Guangdong) can steal a march on competitors.

- Be Patient, but Agile: Capturing these opportunities will not be an overnight play. It may take time to educate the market (e.g. convincing Chinese companies they need an ESG data platform or persuading a local court to use your legal AI tool). Build a realistic timeline and be ready to iterate – perhaps you launch a pilot project or two to demonstrate value. Patience is key: avoid the mistake of withdrawing at the first setback, as the strategic rationale (huge addressable market) remains. That said, remain agile to adjust strategy with policy shifts or market feedback. If a certain sector becomes challenging due to a sudden regulation, pivot focus to a related gap (for instance, if direct ed-tech investment is hard, shift to enterprise training software which is encouraged). Similarly, keep an eye on macro factors – if consumer spending is soft, maybe emphasize B2B opportunities; if a city’s business environment improves (or deteriorates), recalibrate regional focus. Basically, a long-term commitment combined with tactical flexibility will position foreign firms to ride the inevitable ups and downs of the China market while steadily expanding their footprint.

In navigating these steps, foreign investors and firms should lean on their legal and strategic advisors as integral partners. The China market of 2025, with its blend of untapped potential and heightened regulatory oversight, requires a nuanced approach. Those who do their homework, respect the local context, and boldly address China’s market gaps can reap substantial rewards. Foreign law firms and GCs, in turn, have the opportunity to guide this next wave of engagement – steering clients through unfamiliar waters to land on profitable new shores. The message is clear: China’s door to opportunity is open wider than it has been in years – now is the time to step through, with eyes open and game plan in hand.