China’s Economy Faces Stiff Headwinds as Key Indicators Slow in August

New data from China’s National Bureau of Statistics (NBS) confirm that economic momentum waned in August 2025. Industrial output and consumer spending grew at their weakest pace in nearly a year, missing market expectations and underscoring the persistent challenges facing the world’s second-largest economy. These disappointing figures have heightened expectations that Beijing will step up policy support to bolster growth and meet its annual GDP growth target of around 5%.

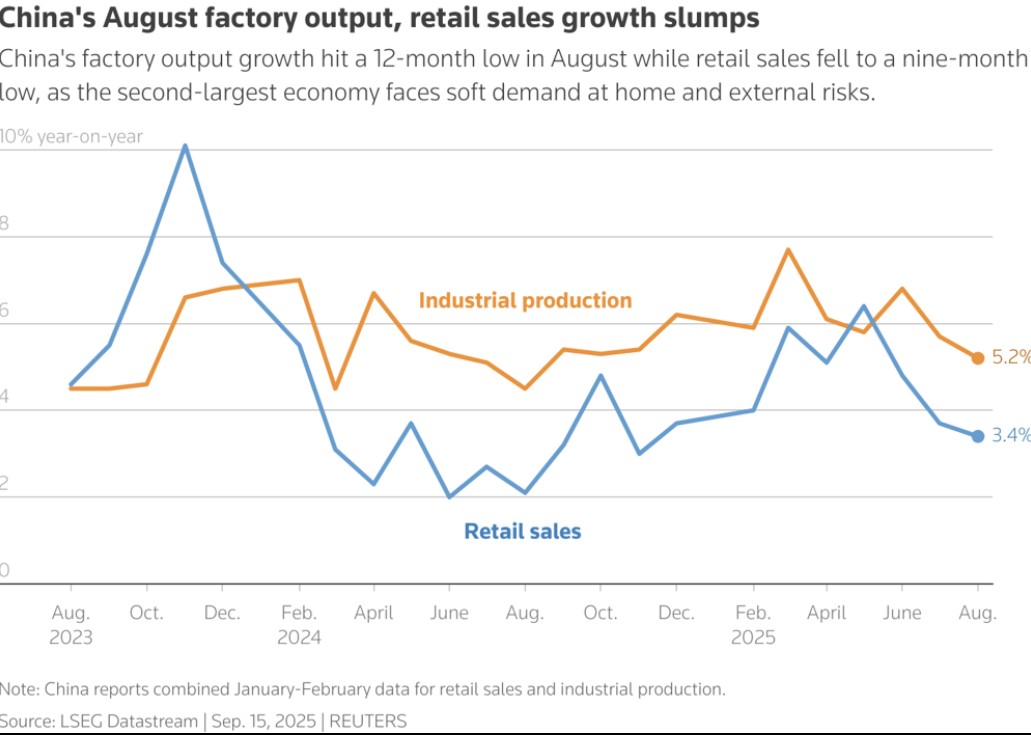

China’s industrial output (orange line) and retail sales (blue line) growth rates have been trending downward over the past year. In August 2025, factory output increased only 5.2% year-on-year — the slowest pace since August 2024 — while retail sales rose just 3.4%, a nine-month low. Both figures came in below analysts’ forecasts, reflecting softer domestic demand amid external pressures.

Key Economic Indicators Weaken in August

Several major indicators pointed to a broad-based slowdown in August, falling short of market expectations:

- Industrial Output: Factory production grew 5.2% year-on-year, the weakest expansion since August 2024. This fell below the 5.7% growth that analysts had forecast and was down from a 5.7% gain in July.

- Retail Sales: Consumer retail sales increased just 3.4% year-on-year – the slowest pace since November 2024 – cooling from a 3.7% rise in July. This too missed expectations (forecast was ~3.9% growth) and highlights sluggish consumer spending.

- Fixed Investment: Fixed-asset investment in the first eight months of 2025 rose a mere 0.5% from a year earlier, a sharp deceleration from 1.6% growth in January–July. This marks the worst investment performance outside of the pandemic period, indicating weak confidence in long-term projects, especially in real estate and infrastructure.

- Unemployment & Housing: The surveyed urban unemployment rate ticked up to 5.3% in August (a six-month high), reflecting an uneven labor market. Meanwhile, China’s housing market remains under pressure – new home prices fell 0.3% in August from the previous month and are down 2.5% year-on-year – a sign of the ongoing property downturn.

Persistent Economic Headwinds

Several persistent headwinds are contributing to China’s slowing momentum and weighed on the August data:

- Prolonged Property Market Slump: China’s real estate sector remains in a deep slump that has lasted for years. New home sales and prices continued to decline in August, with new home prices falling on both a monthly and annual basis. The property downturn – now a multi-year crisis marked by oversupply and developer defaults – has eroded household wealth and strained local government finances. This ongoing property crisis is a major drag on growth, offsetting gains in other areas of the economy.

- Weak Consumer Spending and Confidence: Chinese households are spending cautiously amid an uncertain job market and waning confidence. Retail sales growth has lost momentum despite earlier government efforts (like subsidies for car and appliance purchases) intended to spur consumption. Those subsidy programs have largely run their course, contributing to the recent pullback in consumer spending. Additionally, an “uneven” labor market – exemplified by rising unemployment – has led consumers to tighten their belts, further damping domestic demand.

- External Trade Pressures: Export demand has softened due to weak global conditions and trade frictions. China’s shipments to major markets have been declining; notably, exports to the United States have fallen at double-digit rates for several consecutive months amid ongoing U.S.–China trade tensionsatlanticcouncil.org. While some manufacturers have managed to redirect exports to Southeast Asia, Africa, and Latin America, external uncertainties still pose a headwind. Slower export growth, combined with geopolitical uncertainties, is limiting one of China’s traditional growth engines and adding to the challenges for factories.

Policy Outlook – Balancing Stimulus and Stability

The latest sluggish data have prompted renewed calls for Beijing to ramp up economic support measures. Analysts are closely watching how Chinese policymakers respond in order to shore up confidence and ensure the ~5% GDP growth target remains achievable. Several avenues of potential policy action are under consideration:

- Monetary Easing: The People’s Bank of China may further ease monetary policy. Many economists anticipate modest interest rate cuts (for example, a 10 basis-point cut to benchmark lending rates) and possibly a reduction in banks’ reserve requirement ratio (RRR) to inject liquidity. Incremental rate cuts have already been implemented this year, and additional moves could help lower financing costs for businesses and consumers.

- Fiscal Stimulus: Fiscal authorities could step up spending to stimulate demand. This might include accelerating infrastructure projects and front-loading local government bond issuance to fund investment. Top officials have signaled willingness to “make full use” of fiscal and monetary tools to achieve the annual growth goals, which suggests further government spending or tax support (on top of existing measures) may be deployed in coming months.

- Targeted Support Measures: The government may expand targeted programs to bolster key weak spots. Possibilities include renewed consumer subsidies (to encourage big-ticket purchases), measures to support the troubled housing market (such as looser homebuying restrictions or assistance for developers), and initiatives to boost employment. Beijing has already tried several targeted steps – from small rate cuts to consumer voucher programs and easing some housing policies – but so far these have had limited impact on reversing the downturn. Any new support will likely aim to more directly stimulate household spending and restore confidence.

While additional stimulus now appears more likely, Chinese policymakers must calibrate their response carefully. Not all experts expect an aggressive stimulus deluge: some note that, despite the August slump, conditions are not yet weak enough to force massive intervention. Authorities are wary of exacerbating financial risks – such as high local government debt or asset bubbles – with too much easy credit. Moreover, deep structural issues (from the property overhang to an aging workforce) continue to constrain the effectiveness of short-term policy boosts.

China’s economy is contending with stiff headwinds, and the latest data underscore the delicate balancing act facing Beijing. The government is expected to introduce further policy support to prevent a sharper slowdown, but whether these measures can overcome the persistent challenges – in property, consumer sentiment, and external demand – remains an open question. Analysts will be watching upcoming data and policy announcements closely to gauge if China can regain momentum and finish the year on target.