China Eases Rules for Foreign Investors as Inbound FDI Declines

BEIJING – September 19, 2025: A notable drop in foreign direct investment (FDI) into China this year is spurring Beijing to introduce new incentives and regulatory reforms to lure overseas capital. In the first half of 2025, inbound FDI fell by double digits – official data show FDI inflows of ¥358.2 billion (~$50 billion) from January to May, down 13.2% year-on-yearreuters.com. This slide comes amid global economic uncertainties and US-China tensions, which have made some multinationals cautious about expanding in China. Faced with this challenge, Chinese authorities are moving assertively to “optimize the foreign investment environment”, reducing barriers and sweetening terms for international companieswhitecase.comwhitecase.com.

A cornerstone of the new approach is greater market access. Late last year, China updated its Foreign Investment Negative List (2024), removing all foreign equity caps in the manufacturing sectorwhitecase.com. This historic opening means industries from autos to chemicals are now fully accessible to foreign investors – a stark contrast to past decades when joint ventures were mandatory in key manufacturing fields. Building on that, in March 2024 the State Council issued an Action Plan for High-Level Opening-Up that pledges tax breaks, streamlined approvals, and fair competition safeguards for foreign enterpriseswhitecase.com. Then in July 2025, a multi-agency notice rolled out measures to encourage foreign companies to reinvest their profits back into Chinareuters.com. These measures include tax deferrals/exemptions on reinvested earnings, easier cross-border profit transfers, and support for foreign firms to expand or acquire local companiesreuters.comreuters.com. Local governments are setting up “reinvestment project databases” to match foreign capital with local opportunities, offering services to expedite land leases and permittingreuters.com. At the national level, regulators have simplified procedures for foreign investors to raise funds domestically (for example, easing rules on foreign shareholder loans and Panda bond issuance for reinvestment)reuters.com.

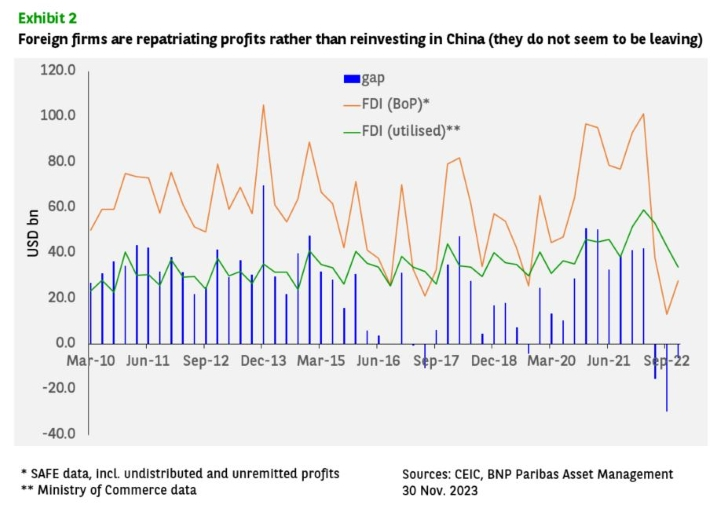

These efforts come at a critical time. Not only has FDI volume dipped, but the composition of foreign investment is shifting. Investment from some Western firms has slowed, especially in sectors where geopolitical frictions and export controls are at play (such as semiconductors and defense-related tech). The United States recently finalized rules to restrict outbound U.S. investments in Chinese advanced tech like AI and chipsreuters.com, which could curb American venture capital flows into China’s tech startups. Meanwhile, EU-China investment relations are under review amid mutual security concerns. In response, China is courting other sources of FDI: capital from the Middle East, ASEAN, and multinational funds not bound by Western restrictions. Officials highlight growing investments in areas like new energy (e.g., foreign automotive battery plants) and financial services after China’s removal of foreign ownership limits in banking, insurance, and asset management. Indeed, several global asset managers have recently obtained full control of their China mutual fund ventures, a direct result of these liberalizations.

[Begin market data] The impact of China’s pro-FDI measures is gradually materializing in data. While headline FDI is down, the number of newly established foreign-invested enterprises rose ~25% YoY in H1 2025, indicating continued interest in smaller-scale ventures even as mega-projects lag. Sector-wise, high-tech industries now account for over 30% of FDI, up from 25% a year ago, suggesting that incentives in tech and green sectors are gaining traction. For example, FDI in high-tech manufacturing jumped 5.9% in H1, with major investments in EV battery factories and pharmaceutical plants (even as overall manufacturing FDI fell)china-briefing.com. Geographically, pilot free trade zones (FTZs) and large cities are drawing a disproportionate share: Shanghai, for instance, saw FDI inflows rise slightly, thanks to financial sector openings and FTZ policies, even as nationwide FDI fell. [End market data]

Industry implications: These trends carry significant strategic implications for law firms, corporate investors, and business executives. On one hand, new market openings mean new deal opportunities. Lawyers are already busy advising clients on taking advantage of China’s eased ownership rules – e.g., helping automakers increase stakes in joint ventures to 100%, or navigating approvals for wholly foreign-owned manufacturing entities in sectors like aviation and heavy equipment. M&A activity is poised to pick up as foreign firms can now pursue strategic investments in Chinese listed companies with lower thresholds (under revised rules, foreign investors can make tender offers and use share swaps, with reduced lock-up periods)whitecase.com. International private equity is examining these channels to potentially acquire bigger positions in China’s growth companies under the updated 2024 regulations.

At the same time, compliance and risk management remain paramount. The regulatory reforms, while positive, still require navigation of China’s bureaucracy. Foreign investors must stay attuned to national security reviews and compliance checks – the Foreign Investment Security Review (FISR) process remains in place for investments in sensitive sectors (technology, data, agriculture, etc.), and enforcement of anti-sanctions and data laws could complicate certain deals. General counsels must evaluate transactions not just for Chinese approval, but also for home country restrictions (as seen with the new U.S. outbound investment screening). For instance, a U.S. or EU company investing in a Chinese AI firm must ensure it doesn’t trigger their domestic prohibitions, even if Chinese law welcomes the capital. This dual compliance landscape is giving rise to intricate deal-structuring – using third-country subsidiaries or delineating business scopes – to thread the needle between jurisdictions.

Market gaps: Importantly, the FDI downturn has revealed gaps that China is eager for foreign players to fill. One gap is in advanced manufacturing expertise: with manufacturing fully open, China seeks foreign technological know-how in areas like semiconductor equipment, aerospace components, and biotech manufacturing. Another gap is capital for innovation – Chinese startups in fields facing U.S. export controls (chips, quantum tech) need investment, and China is offering incentives (e.g., tax breaks, government co-investments) to non-U.S. investors who step in. There are also regional gaps: China is encouraging foreign firms to invest in central and western regions via preferential policies (like special economic zones, tax holidays), aiming to spread investment beyond coastal hubs. Legal advisors are guiding clients through these regional incentive packages and the contractual nuances of deals with local authorities.

Closing insight: China’s message to global investors in 2025 is clear: “We are open for business – on improved terms.” The spate of FDI-friendly policiesreuters.comreuters.com, from broader market access to profit repatriation conveniences, underscores Beijing’s commitment to stabilizing foreign investment amid a challenging geopolitical environment. For multinational corporations and investment funds, this creates a window of opportunity, albeit one that must be approached judiciously. Due diligence remains key – investors should leverage professional services to navigate the evolving legal frameworks, including the new Company Law amendments, sectoral guidelines, and digital security laws that could impact joint operations. The firms that succeed will likely be those that align their investments with China’s strategic priorities (high-tech, sustainability, consumer sectors) and build strong compliance systems to manage political risks. The FDI landscape is becoming more nuanced: no longer just about market size, it’s about market alignment and regulatory acumen. If China’s reforms continue and global tensions don’t drastically worsen, we may see a rebound in FDI flows in 2026 – but targeted to where the opportunities and openings now lie. In the interim, foreign businesses should engage proactively with Chinese policymakers (through chambers of commerce, dialogues) to voice concerns and shape a fair operating environment, while seizing the strategic openings these new policies provide.